Canada's December Rate Decision and the Housing Market

As the Bank of Canada (BoC) prepares to announce its next interest rate decision on December 11th, the market is abuzz with speculation. While the consensus among economists leans towards a rate cut, the magnitude of the reduction—a quarter-point or a half-point—remains a subject of debate.

A Double-Edged Sword

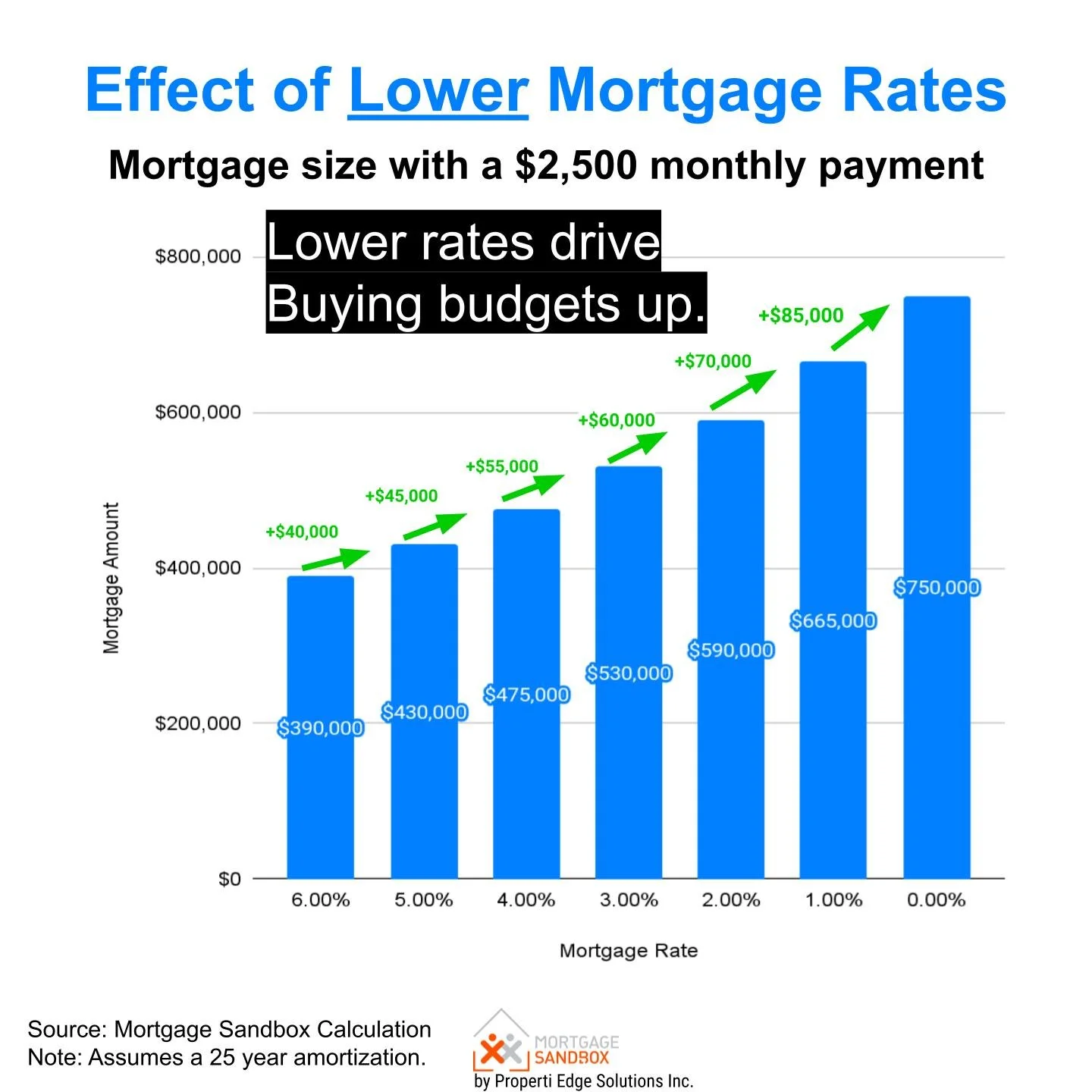

The recent decline in both variable and fixed mortgage rates, averaging around 1.5%, has undoubtedly boosted home buying budgets.

However, this increased purchasing power may not translate into improved affordability.

In a tight housing market characterized by limited supply and intense competition, higher pre-approved mortgage amounts will likely fuel bidding wars, driving up property prices. As a result, the bidder with the deepest pockets will win — and the same bidder wins with higher or lower rates because low rates are available to everyone. Lower rates result in the winning bidder paying a higher purchase price, incurring larger property transfer taxes, and taking on a larger mortgage debt.

A Diverging Path for Variable and Fixed Rates

Looking ahead, variable rates have the potential to decline further as the BoC continues its easing cycle. In contrast, 5-year fixed rates may stabilize within a range of 4.5% to 5%. This divergence can be attributed to the inverted yield curve, a phenomenon where short-term interest rates exceed long-term rates.

Historically, long-term rates tend to be higher than short-term rates. As the BoC lowers short-term rates, the impact on long-term rates may be more muted.

Headline Hype vs. Reality

The market's reaction to the BoC's rate decision may lead to misleading headlines suggesting a significant improvement in housing affordability. However, the reality may be more nuanced. Unless Canada enters a recession, which could trigger a more aggressive rate-cutting cycle, the anticipated rate reductions may not be sufficient to alleviate affordability pressures.

A Soft Landing or a Recession?

The BoC's current economic outlook envisions a "soft landing," a scenario where inflation gradually subsides without triggering a recession. However, if the economic conditions deteriorate, forcing the central bank to adopt a more accommodative monetary policy, further rate cuts could be on the horizon.

In conclusion, while the upcoming rate decision offers a glimmer of hope for potential homebuyers, the true impact on affordability remains uncertain. The interplay between interest rates, housing supply, and economic conditions will ultimately determine the trajectory of the Canadian housing market.